Let’s clear something up right away: you don’t need a traditional 9-to-5 job to get approved for a car loan. I know what you’ve heard—friends telling you lenders won’t look at you without full-time employment, internet forums claiming part-time workers are automatically denied, or dealership finance managers shaking their heads when you mention your work schedule. Here’s the truth that might surprise you: lenders don’t care about your job title or how many hours you work. They care about one thing—can you afford the monthly payment?

The automotive lending landscape has evolved dramatically over the past decade. Banks, credit unions, and finance companies have adapted to the reality that millions of Americans earn solid, reliable income outside traditional employment structures. Whether you’re working 25 hours a week at a retail job, bartending three nights weekly, driving for rideshare services, or juggling multiple part-time positions, you absolutely can qualify for auto financing.

The key is understanding what lenders actually evaluate when reviewing your application. They’re running calculations based on income stability, debt obligations, and credit history—not making moral judgments about your employment status. A part-time worker earning $2,000 per month with minimal debt and good credit is a better lending risk than a full-time employee making $4,000 per month who’s maxed out credit cards and has a history of late payments.

1.2 The Current Landscape of Auto Financing

The gig economy, flexible work arrangements, and the normalization of multiple income streams have fundamentally changed how lenders assess applications. According to recent labor statistics, nearly 27 million Americans work part-time, and millions more combine part-time jobs with freelance work, contract positions, or side businesses. Lenders who refused to work with non-traditional employment situations would be turning away a massive portion of the market.

This shift has been accelerated by improved data analytics. Modern underwriting systems can evaluate income patterns with much greater sophistication than the old binary “full-time or nothing” approach. If you’ve been consistently earning $1,800 monthly from your part-time position for the past year, the algorithm recognizes that pattern as reliable income—even if you’re only working 28 hours per week.

That said, part-time workers do face additional scrutiny. Lenders perceive part-time employment as inherently less stable than full-time positions, which means your application needs to be stronger in other areas to compensate. Understanding exactly what they’re looking for—and how to present your financial situation in the best possible light—makes the difference between approval and rejection.

1.3 What You Will Learn in This Guide

This guide will walk you through everything you need to know to successfully secure auto financing with part-time income. We’ll cover the specific income thresholds lenders require, how debt-to-income ratios work (and why they matter more for you than full-time employees), and the documentation you’ll need to prove your income. You’ll learn practical strategies like leveraging larger down payments, when co-signers make sense, and which types of lenders are most likely to approve your application.

By the end, you’ll understand exactly how to position yourself as a strong candidate despite part-time employment status, the red flags that will get you denied, and the realistic expectations you should have about rates, terms, and vehicle choices. Let’s get started.

2. The Core Question: Can You Get Approved with Part-Time Income?

2.1 The Short Answer: Yes, But With Conditions

The straightforward answer is yes, you can absolutely get approved for a car loan with part-time income. Thousands of part-time workers successfully finance vehicles every month. However—and this is the important caveat—approval comes with conditions that don’t apply as strictly to full-time applicants.

First, you’ll need to demonstrate consistent monthly income that meets minimum thresholds (typically $1,500-$2,000 gross per month, which we’ll discuss in detail). Second, your debt-to-income ratio needs to be excellent, generally below 40-45% including your new car payment. Third, you’ll likely need decent credit (ideally 650 or higher, though subprime options exist for lower scores). And fourth, you need documentation proving all of the above.

The application process takes longer for part-time workers because lenders do additional verification. Where a full-time employee might get instant approval through automated underwriting, your application might go to a human underwriter who manually reviews your pay stubs, bank statements, and employment history. This isn’t rejection—it’s just additional due diligence.

You should also expect that the range of vehicles you can finance may be narrower than for higher-earning applicants. Lenders are unlikely to approve a part-time worker earning $2,000 monthly for a $45,000 SUV, but a reliable $15,000-$20,000 used sedan? Absolutely achievable with the right financial profile.

2.2 Why Lenders Are Hesitant (and How to Reassure Them)

Let’s think like a lender for a moment. When you approve a five-year auto loan, you’re betting that the borrower will make 60 consecutive monthly payments. The biggest risk to that bet is income disruption—the borrower loses their job, has hours cut, or faces unexpected expenses that make the payment unaffordable.

From the lender’s perspective, part-time positions carry higher income disruption risk. Part-time workers are often first to have hours reduced during slow business periods. Part-time positions may not offer the same job protections as full-time roles. And part-time income, by definition, represents a smaller financial cushion if unexpected expenses arise.

This isn’t personal—it’s statistical risk assessment. Your job is to counteract these concerns with evidence that your income is stable and sufficient. Here’s how:

- Show employment longevity: If you’ve been at the same part-time job for 18 months or two years, that demonstrates stability and reduces concerns about sudden job loss.

- Prove consistent income: Providing 3-6 months of pay stubs showing stable earnings (same hours, same pay rate) proves your income isn’t volatile.

- Demonstrate financial responsibility: A strong credit score proves you manage the money you do have responsibly, which matters more than the absolute amount you earn.

- Offer a substantial down payment: Putting 15-20% down reduces the lender’s risk exposure and shows you’ve successfully saved money despite part-time income.

The more of these boxes you check, the more comfortable a lender becomes with your application. You’re essentially building a case that while your employment structure is non-traditional, your financial reliability is rock-solid.

3. The “Big Three” Factors Lenders Look For

3.1 Consistent Monthly Income: The $1,500 to $2,000 Rule

Most auto lenders have minimum monthly income requirements, and the magic number typically falls between $1,500 and $2,000 in gross monthly income. Notice I said “gross”—that’s before taxes and deductions, which is how lenders calculate income. Whether you’re earning that from 40 hours a week or 25 hours a week is irrelevant to the underwriting algorithm.

Let’s break down what this looks like in practical terms. If you’re earning $15 per hour working 25 hours weekly, your monthly gross income is approximately $1,625 ($15 × 25 hours × 4.33 weeks). That clears the minimum threshold at most lenders. If you’re making $12 per hour at 30 hours weekly, you’re at roughly $1,559 monthly—just barely qualifying.

Hourly Rate × Hours per Week × 4.33 = Gross Monthly Income

Example: $14/hour × 28 hours/week × 4.33 = $1,697/month

The “consistent” part is equally important. Lenders want to see that your income has been stable over time, typically requiring at least 3-6 months of pay history at your current income level. If you just started a part-time position three weeks ago, even if you’re earning $2,000 monthly, lenders will be hesitant because there’s no track record.

If your base income from one part-time job doesn’t quite hit the threshold, don’t panic. Many lenders will consider combined income from multiple part-time positions, though you’ll need to document each job separately (more on that in Section 5).

3.2 Employment Stability and History

Time on the job matters tremendously for part-time workers. While a full-time employee might get approved after three months at a new position, part-time applicants typically need to show at least 6-12 months of employment history at their current job to be taken seriously.

Why the longer timeline? Lenders want evidence that your part-time position is genuinely stable, not just a temporary gig. Anyone can work somewhere for two months; demonstrating that you’ve maintained the same position for a year or more shows reliability.

Here’s what strengthens your employment profile:

- Same employer for 12+ months: Ideal scenario—shows you’re an established, valued employee unlikely to lose your position suddenly.

- Consistent hours: If you’ve been working 25-30 hours weekly for the past six months, that’s better than fluctuating between 15 and 35 hours, even if the average is the same.

- Same industry experience: If you’ve worked in retail for three years across two part-time positions, that’s better than jumping from restaurant to warehouse to office jobs.

Conversely, frequent job changes are a red flag. If you’ve had four different part-time jobs in the past 18 months, lenders will question whether you’ll still be employed six months into a 60-month loan term. Even if you have legitimate reasons for the changes, the pattern signals instability from a lending perspective.

3.3 Credit Score: The Trust Meter

Your credit score becomes even more critical as a part-time worker because it compensates for the perceived risk of your employment situation. A credit score of 680 or higher significantly improves your approval odds and access to better interest rates. Scores in the 720+ range can sometimes overcome even marginal income situations.

720+

Prime Rates Available

650-719

Good Approval Odds

600-649

Subprime Territory

<600

Difficult/High Rates

Think of your credit score as proof that you manage money responsibly despite having less of it. When a lender sees a part-time worker with a 740 credit score, they’re seeing someone who consistently pays bills on time, doesn’t overextend themselves with debt, and treats financial obligations seriously. That’s exactly the borrower profile they want.

On the flip side, combining part-time income with a low credit score (below 620) creates a challenging application. You’re asking lenders to take on significant perceived risk—both income instability and demonstrated credit management issues. It’s not impossible, but you’ll face high interest rates (potentially 15-20% APR or more) and may need substantial down payments or co-signers.

If your credit score needs work, consider delaying your car purchase by 3-6 months while you improve it. Pay down credit card balances, ensure all bills are paid on time, and correct any errors on your credit reports. Even a 40-50 point improvement can mean the difference between denial and approval, or between a 14% rate and an 8% rate.

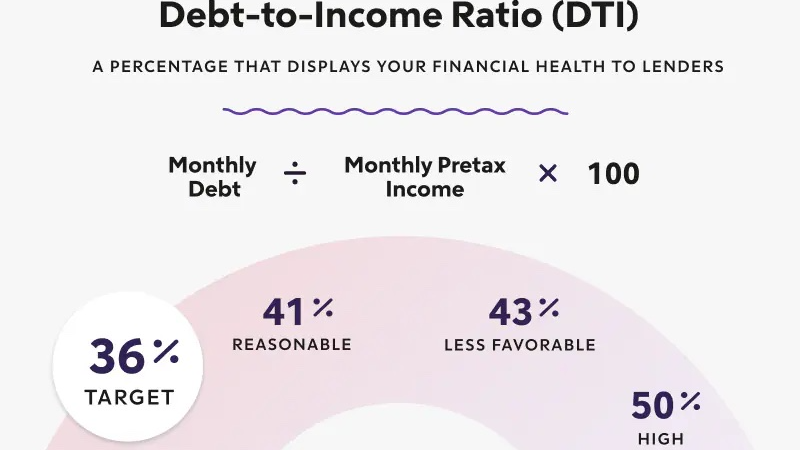

4. Understanding Debt-to-Income Ratio (DTI): The Secret Math

4.1 What Is DTI and Why Is It Critical for Part-Timers?

If there’s one metric you need to understand cold, it’s your Debt-to-Income ratio (DTI). This is the percentage of your gross monthly income that goes toward paying debts, and it’s arguably the most important number in your entire application as a part-time worker.

Lenders use DTI to answer one critical question: after paying your existing debts plus this new car payment, will you have enough money left over for living expenses? The lower your DTI, the more financial breathing room you have, and the more comfortable a lender feels approving your loan.

For part-time workers, DTI scrutiny is intense because you’re starting with a smaller income base. A $400 car payment represents 20% of a $2,000 monthly income but only 10% of a $4,000 income. Every dollar of existing debt you carry takes a bigger bite out of your available income, making the new car payment look riskier.

4.2 How to Calculate Your Own DTI

Calculating DTI is straightforward math that you should do before ever applying for a loan. Here’s the formula:

DTI = (Total Monthly Debt Payments / Gross Monthly Income) × 100

What Counts as Monthly Debt:

- Car loan payments (existing vehicles)

- Student loan payments

- Credit card minimum payments

- Personal loan payments

- Mortgage or rent (some lenders include this, others don’t)

What Doesn’t Count:

- Utilities (electric, water, internet)

- Insurance (health, car, renters)

- Groceries, gas, entertainment

- Phone bills

Let’s work through a real example. Suppose you earn $1,800 gross monthly from your part-time job. Your existing debts include:

- Student loan payment: $150/month

- Credit card minimum payments: $75/month

- Personal loan: $100/month

Your current DTI is: ($150 + $75 + $100) / $1,800 = $325 / $1,800 = 18%

Now you’re shopping for a car that would cost $300/month. Your new DTI would be: ($325 + $300) / $1,800 = $625 / $1,800 = 35%

That 35% DTI is generally acceptable to most lenders, though just barely for part-time income. Understanding this math beforehand helps you shop for vehicles you can actually afford, rather than getting excited about a car only to be denied because the payment pushes your DTI too high.

4.3 The Magic Number: What DTI Do Lenders Want?

Most auto lenders prefer to see DTI ratios below 45-50% including your new car payment. However, for part-time workers, you’ll have better approval odds if you can keep it under 40%, and ideally closer to 35%.

| DTI Range | Lender Perspective | Approval Outlook |

|---|---|---|

| Under 35% | Excellent – comfortable buffer | Strong approval odds, better rates |

| 35-40% | Good – manageable debt load | Good approval chances |

| 40-45% | Acceptable – pushing limits | Possible but scrutinized closely |

| 45-50% | High – limited flexibility | Difficult, may need co-signer |

| Over 50% | Too high – likely denial | Denial or subprime only |

Here’s the practical reality: if you’re a part-time worker earning $2,000 monthly and you keep your DTI under 40%, you’re dedicating a maximum of $800 to debt payments. If you have $200 in existing debt, that leaves $600 for a car payment—which is actually quite reasonable and opens up a decent range of vehicles.

If your DTI is currently high (over 40%), you have two options before applying: pay down existing debts to lower the denominator, or increase your income to raise the numerator. Sometimes waiting 3-4 months while aggressively paying off a credit card or personal loan can dramatically improve your DTI and approval odds.

5. Proving Your Income: The Documentation Challenge

5.1 Pay Stubs vs. Bank Statements

Income verification is where many part-time workers stumble, not because they lack income, but because they don’t have the right documentation prepared. Lenders will require proof of income, and “trust me, I make enough” isn’t acceptable evidence.

The gold standard is pay stubs covering the most recent 30-60 days, ideally showing at least two pay periods. These need to be official pay stubs from your employer showing your name, the employer’s name, gross pay, deductions, and net pay. A handwritten note from your manager won’t cut it.

If your hours fluctuate significantly from week to week—common in retail, hospitality, or seasonal work—pay stubs alone might not tell the full story. A week where you worked 35 hours looks great, but if the next week you only worked 18 hours, the lender sees inconsistency. This is where bank statements become valuable supplementary evidence.

Providing 2-3 months of bank statements showing regular deposits from your employer proves your income pattern over time. Lenders can see your average monthly deposits and verify that you’re consistently bringing in the income level you claimed on your application. This is especially helpful if you’ve been at your job for a while and can demonstrate a stable income pattern.

💡 Pro Tip: Before applying, request your last 3-4 pay stubs from your employer’s HR or payroll department. Many companies provide electronic access through payroll portals. Save these as PDFs and have them ready to submit immediately when requested. Quick documentation turnaround speeds up approval and shows you’re organized and prepared.

5.2 Handling Multiple Part-Time Jobs

Juggling two or three part-time jobs to make ends meet? You’re not alone, and lenders can absolutely work with this situation—but you need to document each income stream separately.

Let’s say you work 20 hours weekly at a retail job earning $800/month, plus 15 hours weekly bartending earning $1,200/month (including tips). Your combined income of $2,000 monthly is solid, but you’ll need to provide verification for both positions:

- Pay stubs from the retail job showing your hourly wages

- Pay stubs from the restaurant showing your base pay

- If tips are a significant portion of income, bank statements showing regular deposits

- Employment verification letters from both employers confirming your position, hours, and length of employment

Some lenders may only count 75-100% of income from your secondary job, especially if you’ve been there for less than six months. The reasoning is that secondary jobs are often the first to be cut if you need to reduce your workload for any reason. If your income from multiple jobs is borderline, factor in this potential discount when calculating what you can afford.

5.3 Tips for Tipped Employees and Commission-Based Roles

If you work in restaurants, bars, salons, or commission-based sales, your income documentation gets more complicated because a significant portion of your earnings doesn’t appear on official pay stubs. A server might have a base pay of $5/hour but actually earn $18-20/hour including tips.

Here’s how to handle this situation:

For tipped employees: Your pay stubs will show declared tips (the portion reported for taxes), but likely won’t reflect your full cash tip income. The best evidence is bank statements showing regular deposits that exceed your official base pay, plus your most recent tax return (Form W-2) showing your total annual earnings including all tips.

For commission-based workers: Pay stubs should show your commission earnings, but because they fluctuate, lenders typically want to see 3-6 months of payment history to calculate an average. If you had one great month earning $3,000 but typically make $1,500-$1,800, they’ll use the lower, more conservative average.

⚠️ Important: Never exaggerate your income on an application, especially with tips and cash earnings. Lenders will verify everything, and discrepancies between what you claim and what you can document is an instant denial—plus potential fraud concerns that could affect future applications.

The most credible approach is providing your previous year’s tax return (if you’ve been at the job that long) which shows your actual total income including tips and commissions as reported to the IRS. This is considered highly reliable documentation because it’s verified income you’ve already reported to federal authorities.

6. Strategies to Boost Your Approval Odds

6.1 The Power of a Large Down Payment

If I could give you one single strategy that dramatically improves your approval odds as a part-time worker, it’s this: save up a substantial down payment. Putting down 15-20% (or more) of the vehicle’s purchase price transforms your application from marginal to strong.

Here’s why down payments are so powerful. First, they reduce the amount you need to finance, which lowers your monthly payment and improves your debt-to-income ratio. A $15,000 car with $3,000 down means financing $12,000 instead of the full amount—maybe $220/month instead of $280/month over 60 months.

Second, down payments reduce the lender’s risk exposure. If you put $3,000 of your own money into the car, you have significant “skin in the game.” You’re far less likely to default and walk away from a loan where you’ve invested substantial personal funds. The lender knows this, which makes them more comfortable approving your application.

Third, a large down payment prevents you from being “upside down” on the loan (owing more than the car is worth). New cars depreciate 20-30% in the first year, so financing the full purchase price means you immediately owe more than you could sell the car for. That’s risky for lenders. A 20% down payment provides a cushion that keeps you at or near even with the vehicle’s value throughout the loan.

💡 Smart Strategy: If you’re currently working part-time and know you’ll need a car in 6-12 months, start aggressively saving for a down payment now. Even putting aside $200-$300 monthly gives you $2,400-$3,600 when you’re ready to buy—enough to make a real difference in your approval odds and payment amount.

6.2 The Co-Signer “Cheat Code”

Adding a creditworthy co-signer to your loan application is like having someone with excellent credit and stable income vouch for you financially. It’s incredibly effective for getting approved, but it comes with serious responsibilities you both need to understand.

A co-signer is someone (usually a parent, family member, or trusted friend) who agrees to be equally responsible for the loan. If you miss payments or default, the lender can pursue the co-signer for the full amount. The loan appears on both your credit report and theirs, and both of your credit scores will be impacted by payment history—positive or negative.

From a lender’s perspective, a co-signer with strong income and good credit eliminates most of their concerns about your part-time status. They’re essentially approving two borrowers instead of one, knowing they have recourse if you can’t pay. This often unlocks better interest rates and higher loan amounts than you could qualify for alone.

The downsides are significant, though. You’re asking someone to take on substantial financial risk for your benefit. If you lose your job or face financial hardship and can’t make payments, your co-signer is legally obligated to cover them—potentially damaging your relationship. Co-signers also tie up their own borrowing capacity; the car loan counts against their debt when they apply for mortgages or other credit.

⚠️ Co-Signer Reality Check: Only ask someone to co-sign if you’re absolutely confident you can make every payment on time for the entire loan term. Missing payments doesn’t just hurt you—it damages their credit and potentially their finances. If there’s any doubt, don’t put someone you care about in that position.

6.3 Choosing the Right Car: Needs vs. Wants

Part-time workers need to be ruthlessly practical about vehicle selection. This isn’t the time to stretch for a dream car or worry about impressing anyone. You’re shopping for reliable, affordable transportation—period.

The sweet spot for most part-time workers is a used vehicle in the $12,000-$18,000 range, ideally 3-5 years old with under 60,000 miles. This price range offers reliable vehicles with plenty of life left while keeping monthly payments reasonable even with moderate interest rates.

Let’s look at the math. A $15,000 car with $2,000 down at 8% APR over 60 months is roughly $260/month. On $2,000 monthly income with minimal other debt, that’s a manageable 13% of your gross income. Compare that to a $28,000 car at $480/month—that’s 24% of your income before considering insurance, gas, and maintenance.

Focus on vehicles known for reliability: Honda Civic, Toyota Corolla, Mazda3, Hyundai Elantra, or compact SUVs like the Honda CR-V or Toyota RAV4. These models hold value well, have lower insurance costs, and won’t drain your budget with constant repairs.

Avoid luxury brands, high-performance vehicles, and trucks/SUVs unless you genuinely need the capability. They’re more expensive to purchase, insure, maintain, and fuel—all of which strain a part-time budget.

7. Red Flags That Will Get You Denied

7.1 Employment Gaps and Job Hopping

Nothing raises red flags faster for lenders than seeing frequent job changes or employment gaps on your application. If your work history shows you’ve had five different part-time jobs in the past two years, lenders wonder if you’ll still be employed in six months when the car payment is due.

Even if you have legitimate reasons for job changes—the business closed, you moved cities, you were pursuing education—the pattern signals instability from a lending perspective. Underwriters don’t have time to investigate the nuances of each employment change; they see the pattern and assess risk accordingly.

Employment gaps are equally problematic. If you worked steadily for a year, then had a four-month gap, then started your current position three months ago, lenders question what happened during the gap and whether it might happen again. Were you unable to find work? Did you quit without another job lined up? These scenarios suggest financial instability.

⚠️ How to Handle Gaps: If you have employment gaps or multiple job changes, be prepared to explain them on your application or to the underwriter. Valid reasons like returning to school, family medical situations, or industry-wide layoffs are understandable. What you can’t overcome is a pattern of irresponsible job-hopping every few months.

7.2 “Stated Income” vs. Verifiable Income

Here’s a mistake that gets applications denied instantly: exaggerating your income on the application with the assumption that you’ll “explain it later” or that the lender won’t verify.

Every single auto lender will verify your income, especially when they see part-time employment status. If you claim $2,500 monthly income but your pay stubs show $1,600, that’s not a “mistake”—that’s fraud. Even if it’s just optimistic rounding (you occasionally have good weeks that push you to $2,500, but your average is lower), the discrepancy will result in immediate denial.

The days of “stated income” loans where borrowers could claim whatever income they wanted without verification are long gone, especially after the 2008 financial crisis. Modern underwriting requires documentation for every dollar of income you claim.

Be conservative when stating your income. If your income fluctuates, use your average from the past 3-6 months or even your lowest consistent month. Underselling your income slightly is far better than overstating it and getting caught.

7.3 Ignoring Total Cost of Ownership

Here’s a reality check many first-time buyers miss: the car payment is only one part of the cost. Lenders know this, and they’re evaluating whether you can afford not just the loan, but also insurance, gas, maintenance, and repairs on your part-time income.

A $250/month car payment might seem manageable until you add $150/month for insurance (potentially more for younger drivers or those with poor credit), $100+/month for gas, and $50-100/month for maintenance and unexpected repairs. Suddenly your $250 “car expense” is actually $550-600/month—more than double the payment alone.

Before financing any vehicle, get insurance quotes for that specific make and model with your actual driving record and coverage needs. Research the vehicle’s reliability ratings and average maintenance costs. Calculate your expected monthly fuel expense based on your actual driving patterns. Then add all of this up and honestly assess whether it fits in your budget alongside your other living expenses.

If the total cost of ownership would consume 30-35% or more of your monthly income, you’re looking at the wrong car. Step down to a less expensive, more fuel-efficient, cheaper-to-insure vehicle that won’t financially suffocate you.

8. Where to Look for Financing as a Part-Time Worker

8.1 Credit Unions: The Friendly Option

If you’re a part-time worker seeking auto financing, credit unions should be your first stop. These member-owned financial institutions consistently offer better rates and more flexible underwriting than traditional banks or dealership financing—especially for non-traditional employment situations.

Credit unions take a “relationship banking” approach, meaning they’re more willing to look at your overall financial picture rather than just running your application through an automated underwriting system. A human underwriter might see that while you work part-time, you’ve been a credit union member for five years, maintain a savings account, and have never missed a payment on your credit card. That holistic view works in your favor.

Rates at credit unions typically run 1-3 percentage points lower than banks or dealerships for comparable credit profiles. On a $15,000 loan, that difference saves you $800-$1,500 over the life of the loan—real money that matters on a part-time income.

The main requirement is membership, which usually involves working for specific employers, living in certain geographic areas, or belonging to particular organizations. Many credit unions have broad membership criteria (like “living in X county”), making membership accessible to most people. Even if you need to join a specific association ($10-20 fee) to qualify for credit union membership, it’s worth it for the better financing terms.

💡 Credit Union Strategy: Apply for pre-approval at 2-3 credit unions before you start car shopping. This gives you a committed financing rate and amount, which provides leverage when negotiating at dealerships. You can walk in knowing “I’m pre-approved for up to $15,000 at 6.5% APR—can you beat that?”

8.2 Subprime Lenders and “Buy Here Pay Here” Lots

If your credit is challenged (below 600) or your income situation is particularly difficult, you may end up considering subprime lenders or “Buy Here Pay Here” (BHPH) dealerships. These options can get you approved when traditional lenders won’t, but they come with significant trade-offs.

Subprime lenders specialize in high-risk borrowers, charging interest rates that reflect that risk—typically 12-20% APR or even higher. On a $12,000 loan at 18% over 60 months, you’ll pay over $5,000 in interest alone—nearly half the cost of the car. These loans also often include strict terms, larger down payment requirements, and vehicles with GPS tracking devices that can disable the car if you miss payments.

Buy Here Pay Here lots are dealerships that finance their own vehicles rather than using traditional lenders. They typically cater to customers with very poor credit or unstable income. While approval is nearly guaranteed, the vehicles are often overpriced, interest rates are astronomical (20-25%+ effective APR), and the quality of the cars is questionable at best.

⚠️ Last Resort Warning: Only use subprime lenders or BHPH as an absolute last resort when you need transportation immediately for work and have no other options. The terms are predatory, and you’ll pay 2-3 times what the car is worth by the time you’re done. If at all possible, save up cash and buy a cheap used car outright rather than getting trapped in these loans.

8.3 Online Lenders and Pre-Qualification

Modern online lenders and lending marketplaces offer a valuable tool for part-time workers: soft-pull pre-qualification. This lets you see what rates and terms you might qualify for without impacting your credit score, allowing you to shop for financing before you shop for cars.

Services like Capital One Auto Navigator, LendingTree, Carvana, and others offer pre-qualification where you enter your basic information (income, employment, estimated credit score) and receive preliminary offers from multiple lenders. Because these use soft credit pulls, they don’t affect your credit score, so you can explore options without consequences.

This is particularly valuable for part-time workers because it helps you understand your realistic financing range before falling in love with a car you can’t actually afford. If pre-qualification shows you’ll likely qualify for $10,000-$12,000 at 11% APR, you know to shop in that price range rather than wasting time looking at $20,000 vehicles.

Once you’ve pre-qualified and have a sense of your options, you can proceed with formal applications at the most promising lenders. These will involve hard credit pulls that temporarily impact your score, but shopping multiple lenders within a 14-day window typically counts as a single inquiry, minimizing the damage.

9. Conclusion

9.1 Summary of Key Requirements

Let’s bring everything together. Can you buy a car with a part-time job? Absolutely—thousands do it successfully every month. The keys to approval are:

- Consistent monthly income of $1,500-$2,000 or more, documented through pay stubs and bank statements showing stable employment for at least 6-12 months

- Debt-to-income ratio below 40-45% including your new car payment, proving you have room in your budget for the additional expense

- Decent credit score (650+), demonstrating you manage limited resources responsibly and are trustworthy with borrowed money

- Thorough documentation of all income sources, employment history, and existing debts to satisfy lender verification requirements

- Realistic vehicle selection that fits your budget and needs rather than wants, keeping total cost of ownership manageable

Strategies that significantly improve your odds include saving a substantial down payment (15-20%), considering a creditworthy co-signer if available, and shopping at credit unions rather than traditional banks or dealerships. Starting with pre-qualification helps you understand your realistic financing range before you fall in love with a car you can’t afford.

9.2 Final Encouragement

Working part-time doesn’t make you a second-class borrower. You’re earning honest income, managing your finances, and deserve access to reliable transportation just like anyone else. The key is understanding what lenders need to see and presenting your financial situation in the strongest possible light.

Take the time to prepare properly. Get your documentation together, calculate your DTI, check your credit score, and save for a down payment if possible. Walk into the financing process informed and confident, knowing exactly what you can afford and what you need to qualify.

The reality is that lenders aren’t looking for reasons to deny you—they’re in the business of making loans and earning interest. If you can demonstrate stable income, manageable debt, and responsible credit history, you’ll find lenders willing to work with you regardless of how many hours you work per week.

Your part-time job might be a stepping stone to full-time employment, a way to balance work with school, or a lifestyle choice that gives you flexibility. Whatever your situation, you can successfully finance a vehicle if you approach the process strategically. Take the insights from this guide, apply them to your specific circumstances, and go get the car you need. You’ve got this.

About This Guide

This comprehensive guide is based on automotive lending industry standards, credit union underwriting practices, and consumer finance regulations as of 2026. Information reflects typical lender requirements, though individual lender policies may vary.

Disclaimer: This guide is for informational and educational purposes only and does not constitute financial or legal advice. Loan approval depends on individual circumstances, lender policies, and market conditions. Always review loan terms carefully before signing any financing agreement.